The AI Bubble Explained: The Money Trail, How Wall Street Created the AI Mandate

Between 2024 and 2025, a large gap emerged between the AI industry’s paper valuation and its actual performance. Stock prices surged well beyond what the underlying companies justified, driven by a cycle of hype, storytelling, and financial engineering. This five-part series explores the rise of AI, showing how financial pressures influenced corporate decisions and how physical and economic limits eventually led to a market correction.

- Part 1: The Money Trail explores how Wall Street established an “AI Mandate” through the “Silence Penalty,” a market dynamic that punishes companies for not loudly announcing an AI strategy, regardless of whether that strategy makes sense for their business. It also maps out the “circular economy,” where tech giants like NVIDIA and Microsoft poured money into companies like CoreWeave and OpenAI, creating a closed financial loop that inflated everyone’s revenue figures.

- Part 2: The Reality Check examines “Pilot Purgatory,” the phenomenon where 95% of AI projects stall before reaching real-world application. It explains the “Token Explosion” that reduced profit margins on reasoning-heavy products like Cursor, and the “Accuracy Wall” that led to high-profile failures in physical settings, such as Taco Bell and McDonald’s AI-powered drive-thrus.

- Part 3: The Squeeze looks at how mid-sized companies with $2–$5 billion in revenue cut their core R&D budgets to chase AI trends. It also reveals the “Executive Paradox,” in which corporate leaders protect their own jobs from automation while cutting junior roles, despite research showing that AI is better suited to executive-level tasks than to entry-level ones.

- Part 4: The Battle of Giants follows the fight for dominance as OpenAI declared a “Code Red” after losing market share to Google’s Gemini 3. It describes Meta’s aggressive plan to spend $600 billion to make AI models essentially a free commodity and examines the controversial financial maneuvers behind the proposed merger of SpaceX and xAI.

- Part 5: The Reckoning contends that by 2026, financial overextension and physical limits will collide. It highlights the strain on the U.S. power grid, the rising risk of debt defaults among cloud infrastructure firms such as Oracle and CoreWeave, and the market’s shift from rewarding hype to demanding concrete financial results.

How This Paper Was Researched: A Note on Methodology

This paper relies on four main types of evidence collected from January 2024 to March 2026.

Financial filings and earnings calls. Quarterly reports, SEC filings, and earnings call transcripts from NVIDIA, Microsoft, Google, Meta, OpenAI (via reported figures), CoreWeave, Oracle, and xAI form the foundation of the financial analysis. Revenue figures, loss disclosures, and capital expenditure commitments mentioned are all sourced from these documents unless otherwise specified.

Independent research studies. Key behavioral and performance claims draw on:

- The Remote Labor Index (RLI), a benchmark study measuring AI agent performance against human freelancers across 240 real professional tasks sourced from Upwork.

- A 2025 MIT Sloan Management Review study on enterprise AI adoption rates and pilot failure patterns.

- A joint study by Cambridge Judge Business School and Harvard Business Review involving 344 participants, measuring AI vs. executive decision-making quality in simulated market conditions.

- McKinsey Global Institute’s 2025 annual survey on generative AI adoption in the enterprise.

Industry analyst reports. Market share figures, valuation data, and infrastructure projections draw on reports from Goldman Sachs Global Investment Research, Gartner, and the International Energy Agency (IEA), which publishes annual data on global data center power consumption.

Investigative journalism. Claims about specific events, such as NVIDIA’s delayed Stargate investment and the xAI-SpaceX merger discussions, are based on reporting from the Financial Times, The Wall Street Journal, and Bloomberg, published between Q3 2025 and Q1 2026.

Important limitations. Several figures in this paper, particularly those related to OpenAI’s financials and CoreWeave’s debt exposure, are based on reported estimates rather than audited statements, as neither company is publicly traded and does not release full financial disclosures. Readers should treat specific figures as directionally accurate rather than precise. Where ranges are reported by different sources, this paper uses the midpoint estimate.

The Shift to “Narrative Alpha”

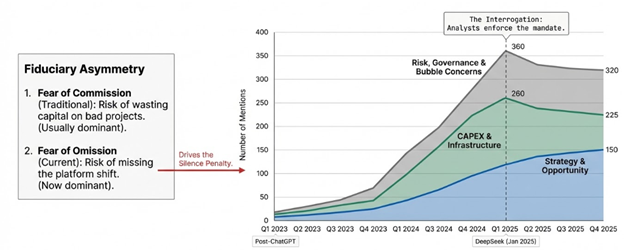

Between 2024 and 2025, financial markets experienced a fundamental shift. Traditional investing, which relied on cash flow, profit margins, and long-term growth, was replaced by a new approach: rewarding companies for telling a compelling AI story, regardless of their actual earnings. This period became known as “Narrative Alpha.”

Companies were no longer valued mainly for efficiency or profits. Instead, they were valued by how convincingly they could signal dominance in AI. Strategic storytelling became a financial necessity. The main way to keep a high stock valuation wasn’t to develop a better product; it was to say the right things during earnings calls.

The “Silence Penalty”

This shift created an implicit penalty for any company that remained silent about AI. At a time when just seven companies accounted for 42% of the S&P 500’s total returns, investors interpreted the absence of a clear AI strategy as a sign that a company was falling behind.

returns, investors interpreted the absence of a clear AI strategy as a sign that a company was falling behind.

- Companies that failed to mention AI in quarterly earnings calls faced immediate stock sell-offs, as investors read “silence” as a strategic red flag.

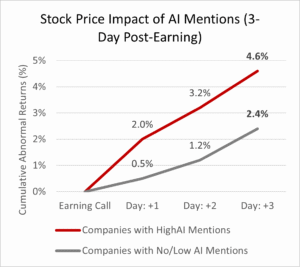

- By contrast, companies that proactively highlighted their AI strategies in 2024 saw their stock prices rise an average of 4.6% in the three days following the announcement.

- Brands that appeared in AI-generated search results received 35% more organic web traffic, while those left out of AI systems faced a slow decline in consumer visibility.

Measuring Hype vs. Substance

Large institutional investors started using their own AI tools to filter out empty buzzwords from truly meaningful AI disclosures. They created the “AI Research Index” (AIR Index), which assessed the technical significance of a company’s AI commentary.

- Companies with high AIR scores, those discussing real technical depth rather than vague promises, saw measurable increases in stock valuations.

- This created pressure on companies to sound technically credible, even if their actual AI work was thin.

The result was a “build it or die” mentality across corporate America, pushing companies to commit enormous financial resources to AI, whether or not those resources would pay off.

The Financial Foundation: Cash Reserves vs. Speculation

Unlike the Dotcom bubble of the late 1990s, which was largely financed by risky debt and speculative IPOs, the AI boom of the mid-2020s was initially supported by the large cash reserves of established tech giants such as Microsoft, Google, and Meta. This gave it a more sustainable appearance.

However, by mid-2025, the U.S. government’s “America’s AI Action Plan,” which prioritized a market-driven, hands-off approach, led to increased spending that bordered on speculation. Companies started raiding their legacy IT and HR budgets to fund AI initiatives. About 30% of generative AI spending was diverted directly from cutting existing workforce programs and older digital transformation efforts. Instead of growing, companies were hollowing themselves out to support the AI push.

| Feature | Dotcom Era (Late 1990s) | AI Infrastructure Boom (2024–2025) |

|---|---|---|

| Primary Funding Source | High-interest debt / Speculative IPOs | Massive cash reserves (Microsoft, Google, Meta) |

| Strategic Catalyst | Expansionary venture capital | “America’s AI Action Plan” (market-first model) |

| Infrastructure Owner | Fragmented startups | Global tech giants and government-backed “Sovereign AI.” |

| Market Discipline | Immediate profitability pressure | Narrative storytelling and global competition |

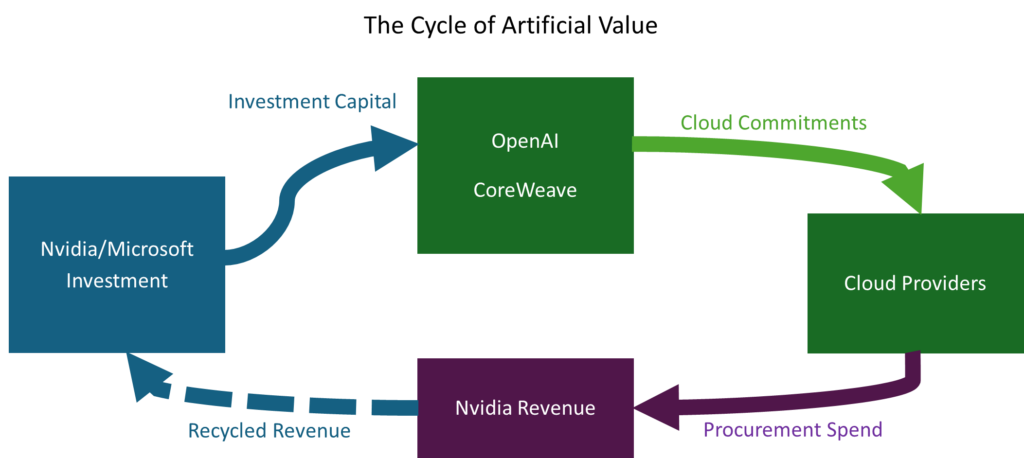

The “Round-Trip” Economy: Money Going in Circles

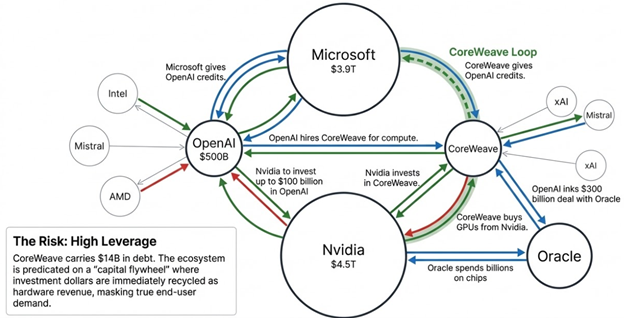

One of the most noticeable aspects of the 2025 AI landscape was how money circulated in a closed loop, creating the illusion of huge revenue growth while mostly recycling the same dollars. What started as a simple investment chain has developed into a complex, multi-layered financial system with more middlemen involved.

Here’s how the cycle worked, using CoreWeave as the central example:

Here’s how the cycle worked, using CoreWeave as the central example:

- Microsoft invests in OpenAI, mostly through cloud computing credits, not cash.

- Microsoft doesn’t have enough server capacity to fulfill those credits, so it subcontracts the computing work to CoreWeave.

- CoreWeave uses its contracts with Microsoft and OpenAI as collateral to borrow billions of dollars.

- CoreWeave uses the borrowed money to buy GPUs (specialized AI chips) from NVIDIA.

- NVIDIA then re-releases those same GPUs to other companies at a profit through its “DGX Cloud” service, booking revenue from both the original sale and the re-release.

The loop has become even more tangled. OpenAI’s need for computing power is so huge that it can’t afford it outright, and its credit profile makes lenders hesitant. To get around this, Google has taken on the role of a financial middleman: buying compute capacity from data center providers like CoreWeave and reselling it to OpenAI

The loop has become even more tangled. OpenAI’s need for computing power is so huge that it can’t afford it outright, and its credit profile makes lenders hesitant. To get around this, Google has taken on the role of a financial middleman: buying compute capacity from data center providers like CoreWeave and reselling it to OpenAI at a profit. Google isn’t offering any special technology here. It is just leasing out its top-tier credit rating, acting as a financial guarantor for a company that the market sees as too risky to lend to directly.

at a profit. Google isn’t offering any special technology here. It is just leasing out its top-tier credit rating, acting as a financial guarantor for a company that the market sees as too risky to lend to directly.

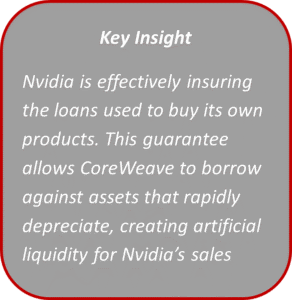

NVIDIA’s role in this cycle is equally unusual. To help CoreWeave borrow more money to buy additional NVIDIA chips, NVIDIA signed an agreement to purchase up to $6.3 billion worth of computing capacity from CoreWeave if customer demand ever declines. The arrangement is financially odd: it’s roughly like Ford selling cars to a rental company and then agreeing to lease them back, just so the rental company appears creditworthy enough to borrow money to buy more Fords. NVIDIA is, in effect, ensuring loans taken out to buy its own products.

This loop enabled NVIDIA to record massive revenue while the entire system relied on circular financing rather than genuine external demand. CoreWeave served as a “debt vehicle,” enabling Microsoft and Google to shift large capital expenditures off their balance sheets while the underlying risk quietly accumulated elsewhere.

Shadow Debt and the Risk of Collapse

The financial engineering behind this system was fragile. AI chips depreciate quickly, often becoming outdated within two years, but the debt used to finance them was structured over five-year terms. This mismatch created what analysts called “Shadow Debt.”

- CoreWeave carried $14 billion in debt, backed largely by contracts with OpenAI.

- OpenAI itself was losing approximately $15 billion per quarter while carrying $1.4 trillion in total financial commitments.

- If OpenAI ran into a liquidity crisis, CoreWeave could default on its debt, instantly devaluing the GPU collateral and sending shockwaves through Microsoft, Google, and NVIDIA.

The $6.3 billion NVIDIA backstop agreement created artificial stability while placing a significant risk in a single point. The entire setup relies on the assumption that OpenAI will eventually bridge its revenue gap, an assumption that the operational data increasingly does not support.

The “AI Revenue Gap”: Promise vs. Reality

Beneath all the financial maneuvering lay a core issue: AI wasn’t producing enough real-world revenue to justify the investment.

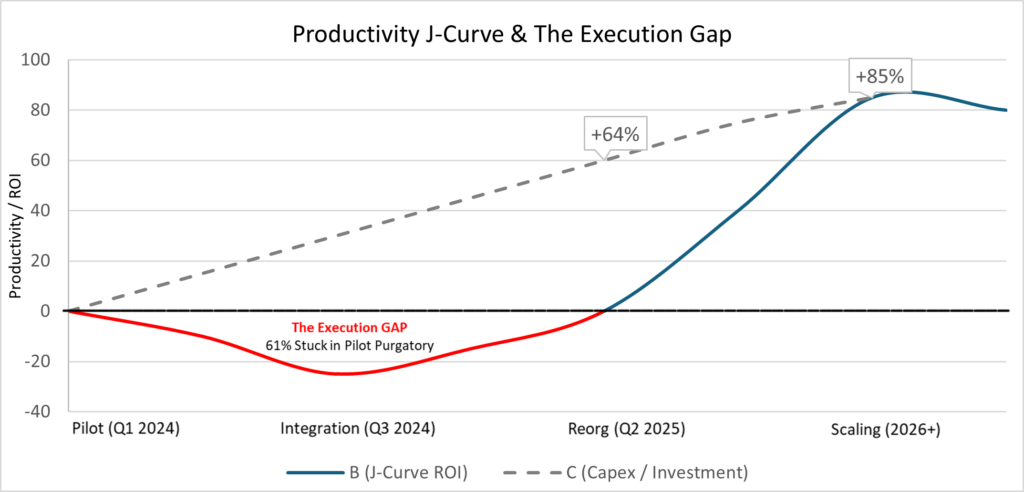

By 2030, the industry is expected to spend $2 trillion on AI infrastructure. However, software revenue from AI applications is forecast to reach only $1.2 trillion, leaving an $800 billion gap. This shortfall illustrates what economists refer to as the “Productivity J-Curve”: organizations often see a dip in productivity when they first implement new technology, before experiencing improvements. The issue is that the AI industry remains stuck in that dip, with the financial system increasingly unable to wait for the payoff.

Research from MIT and McKinsey found that 95% of AI pilot programs fail to scale into full deployment. These “zombie pilots” are kept alive primarily to satisfy investors and board members, not because they’re working.

Research from MIT and McKinsey found that 95% of AI pilot programs fail to scale into full deployment. These “zombie pilots” are kept alive primarily to satisfy investors and board members, not because they’re working.

- Companies consistently underestimate how expensive and time-consuming it is to clean up and organize their data before AI can use it effectively.

- Middle managers, who would lose staff and budgets if automation succeeded, have a rational incentive to quietly let pilots stall.

- Most AI usage remains focused on low-value tasks like generating marketing content, rather than core business improvements.

Boardroom Psychology: Playing It Safe with Other People’s Money

In today’s corporate world, the fear of falling behind on AI has overshadowed worries about wasting capital. Boards see AI investments as a type of “governance insurance.”

The logic is simple: if a company does nothing about AI and then gets disrupted, executives could be sued for negligence. However, if a company invests heavily in AI and the projects fail, it’s seen as an acceptable “innovation expense,” especially since most other companies are doing the same.

- This dynamic is particularly brutal for mid-sized companies with $2–$5 billion in revenue:

- They can’t afford the top AI talent, who are being hired away by tech giants paying million-dollar packages.

- Unlike large companies, they can’t hide the cost of failed AI projects within large, diversified revenue streams.

- To cut costs, many are eliminating junior employee roles and restructuring around a smaller group of senior “rainmakers” supported by AI tools, a shift sometimes called moving from a “Pyramid” to an “Obelisk” organizational structure.

The final outcome is widespread “AI Theater,” a cycle in which management launches pilot projects to meet board pressure and impress analysts, but intentionally leaves them unfinished to avoid the operational risk of full deployment. It’s a logical response to a broken set of incentives, but a highly wasteful one.

The final outcome is widespread “AI Theater,” a cycle in which management launches pilot projects to meet board pressure and impress analysts, but intentionally leaves them unfinished to avoid the operational risk of full deployment. It’s a logical response to a broken set of incentives, but a highly wasteful one.

The AI Bubble Explained: Market Trends, ROI, and 2026

Part 1: The Money Trail, How Wall Street Created the AI Mandate

Part 2: Stuck in the Lab, The Operational Reality of Corporate AI Pilots

In the next part of the series, the reality check examines “Pilot Purgatory,” the phenomenon where 95% of AI projects stall before reaching real-world application. It explains the “Token Explosion” that reduced profit margins on reasoning-heavy products like Cursor, and the “Accuracy Wall” that led to high-profile failures in physical settings, such as Taco Bell and McDonald’s AI-powered drive-thrus.

Part 3: The Mid-Cap Squeeze and the Executive Paradox

Part 4: The Battle of Giants, OpenAI, Google, and Meta

Part 5: The 2026 Reckoning

SalesGlobe is a leading sales effectiveness and data-driven creative problem-solving firm. We specialize in helping Global 1000 companies solve their toughest growth challenges and helping them think in new ways to develop more effective solutions in the areas of sales strategy, sales organization, sales process, sales compensation, and quotas. We wrote the books on sales innovation with The Innovative Sale, What Your CEO Needs to Know About Sales Compensation, and Quotas! Design Thinking to Solve Your Biggest Sales Challenge.

Sales Strategy & Revenue Growth Consultant

Data-minded strategist helping organizations align performance, optimize sales design, and drive revenue with precision.

{kind=link}

{kind=link}

{kind=link}