A 50 Year Mortgage? Is the Next Gen Going to Live Life-as-a-Service?

A 50 Year Mortgage?

Is the Next Gen Going to Live Life-as-a-Service?

What You Need to Know

- ◆Home prices have far outpaced income growth for 40 years and homeownership has become interest rate dependent.

- ◆The first-time buyer is now a 40-year-old compressing the years available to build equity.

- ◆A 50-year mortgage doesn’t fix the economics. It nearly doubles total interest.

- ◆Supply has tightened to a multi-decade low while the number of homes for sale has collapsed relative to population growth.

- ◆Cheaper to rent than buy is a life-as-a-service myth that endangers wealth creation.

- ◆Opportunities abound to help homebuyers improve their positions and help your B-to-B customers in turn.

SalesGlobe Signals is about seeing a bigger, macro view on growth and taking actions that will help you reach your growth aspirations. This month let’s look at some Signals on the housing market that may be impacting your customers – stretched affordability, the rising age of first-time buyers, and the potential for a 50-year mortgage. Underneath it all is our bigger question: If the next generation of buyers never really own in the traditional equity sense, do they start to live life-as-a-service and, from the perspective of your business, how can you help them as customers to get to a better place?

In Signals, our focus is on helping executives answer two questions for their businesses:

- What Are the Market Signals? Indicators you might watch for your business that may signal what's ahead.

- What Does This Mean for Profitable Revenue Growth? Based on the signals, how you may think about growth and the actions you may consider.

The dynamic of the housing market has shifted which may create opportunities for you to help your customers

What Are the Market Signals? Home ownership has been the American dream for nearly one hundred years, at least going back to when mortgages as we know them came into existence. And for much of the world, home ownership is also their aspiration. But a series of factors, or Signals as we call them, have come together to bring that dream to a rude awaking that could leave the next generation paying on the monthly meter rather than reaching financial independence.

Signal 1. The 50-Year Mortgage is Not a Panacea for Home Ownership Affordability.* The 50-year mortgage has moved from fringe idea to policy conversation. Earlier this month, Federal Housing Finance Agency Director Bill Pulte publicly floated the idea of a 50-year mortgage, which has reportedly been discussed with the administration as one tool to address the housing affordability challenge for much of the country. The idea is that, by extending the loan term, the resulting lower monthly payment would give new buyers a path to ownership. For example, on a median home of about $425,000, a traditional 30-year mortgage at 6% interest has a monthly principal and interest payment of about $2,420.

What Does This Mean? With a 50-year mortgage on the same loan, that monthly payment drops to about $2,125. It sounds more attractive if you think of your life in monthly payments, like your car lease. But, for that $300 benefit, the homeowner would pay almost double the amount of total interest over the life of the loan. To bring that into dollar terms, for the example above, total interest over the life of the loan for a 30-year mortgage adds up to $492,312 compared to total interest on a 50-year mortgage of $917,332, a difference of over $425,000.

The buyer could have purchased a second home of the same value with the extra interest. And, with the first-time home buyer now 40 years old, their mortgage burning party would have to be delayed until they reached age 90. Since the average U.S. life expectancy is about 79, the majority of 50-year mortgage holders would likely die in debt, never enjoying being free from monthly payments.

And does the 50-year mortgage solve the monthly payment problem better that a reduction in mortgage rates? The answer is no. If a lower monthly payment is the goal, to get to that monthly payment of $2,237, the mortgage rate would need to drop from 6% to about 4.8%. We were just there in 2021. So, locking in the new homeowner to an additional twenty-year mortgage sentence, when rates could reasonably be back in the range above within a few years seems ludicrous. The borrower functions as a long-term tenant of the bank, paying a monthly fee for the service of shelter, but retaining responsibility for maintenance, taxes, and insurance. It’s up to the people who know these numbers to make the risks clear to the generation of would-be 50-year mortgage victims.

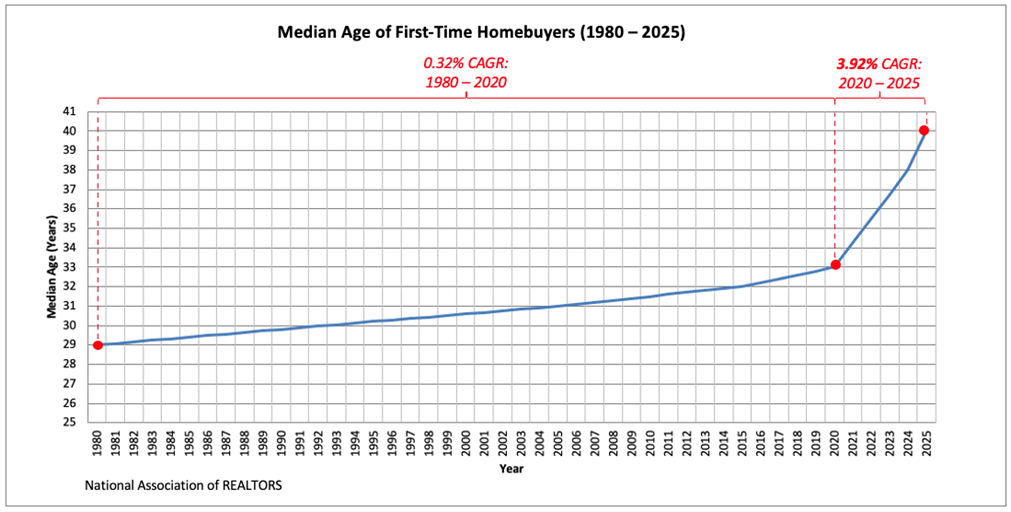

Signal 2. First-Time Home Buyers Are Showing Up Late to the Mortgage Burning Party. I referenced the increasing age of the first-time home buyer above. So, let’s take a brief look. The increasing age of first-time home buyers is where the life-as-a-service risk starts to creep in.

From 1980 to 2025, the median age of the first-time homebuyer has increased from 29 to 40. That in itself appears to be a big jump of 38%. But, breaking that apart in the graph, you may notice a dramatic change around 2020. Between 1980 and 2020, first-time homeowner age increased an average of 0.32% annually. But from 2020 to 2025, first-time homeowner age lept an average of 3.92% annually.

This second trajectory, around 2020, appears to be where median age became unhinged, likely due to factors that include rapid home price inflation, mortgage rate increases (but keep in mind that mortage rates were over 18% in 1981), limited housing supply, investor competition for starter homes, and delayed family formation.

What Does This Mean? The median first-time homebuyer, age 40, has already spent almost the first half of their working life paying for housing as-a-service and are only 25 years from Social Security eligibility. This reduces the number of years to pay down mortgage principal, reduces the number of years to benefit from home asset appreciation, and reduces the amount of home equity the owner will build and access through home equity lines to fund home upgrades, children’s education, and other expenses and investments.

In short, homeowners have something that looks like a “home subscription as a service” that eliminates one path to building wealth and equity that could drive economic growth.

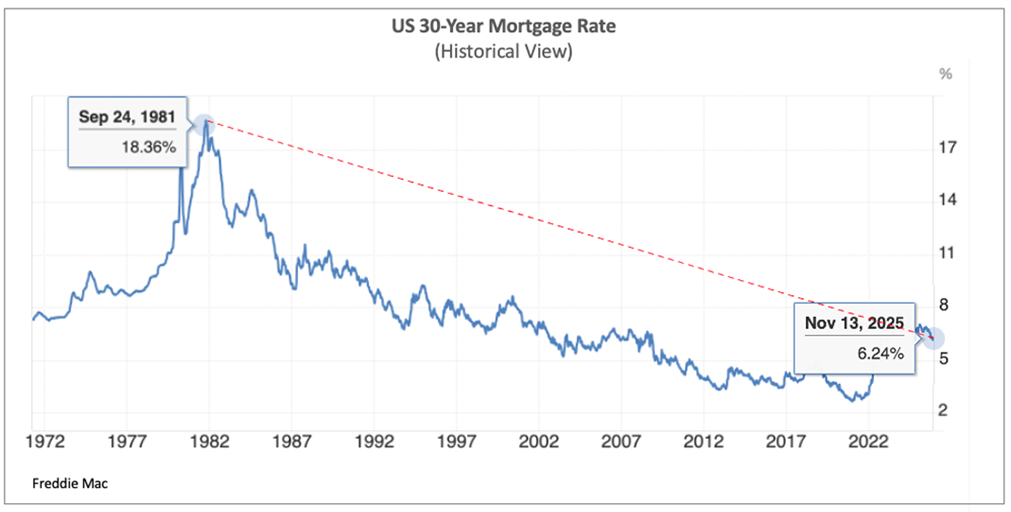

Signal 3. Mortgage Rates Have Increased but Are Low in Historical Context. The current view on mortgage rates is that they are so high they’re impacting homeownership. When we focus on a near-term view of mortgage rates over the past few years, that may be true. But that changes when seen in a bigger context.

What Does This Mean? While the 30-year mortgage at over 6% is 50% higher than the 4% mortgages of 2021, a 6% mortgage rate compared to the 18% mortgages of 1981 is the deal of the half century. Mortgage rates have steadily declined since 1981 which has fueled home ownership as well as many other forms of business and personal investment. Lower rates and easy money also led to a boom in lending with looser lending standards that erupted in the 2008 financial crisis. But the overall trend has been toward lower rates increasing affordability of mortgages.

For more on the Federal Funds rate in context, see our SalesGlobe Signals August Issue, "How Will Interest Rate Changes Impact Your Customers and Your Opportunities?"

Signal 4. Home Ownership Affordability Has Become More Interest Rate Dependent Than Price Dependent Over Time. When we look at the affordability of home ownership over a period of years, we see two views that, together, reveal a shift in what makes homeownership affordable.

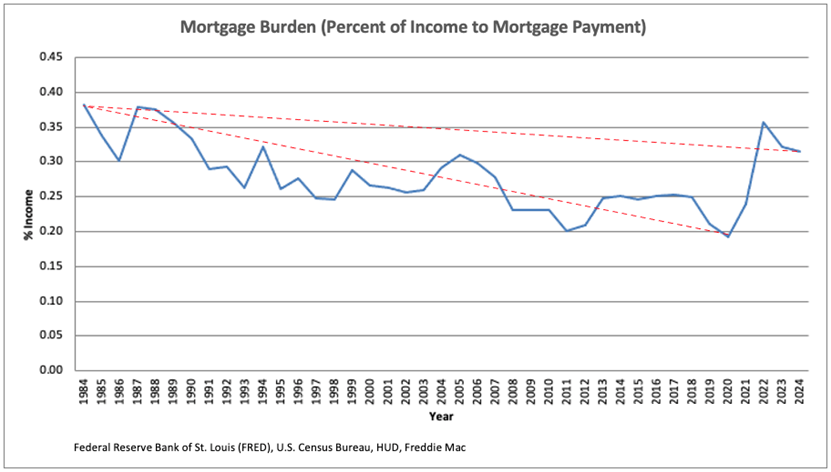

Mortgage burden, the percent of income required to pay the principal and interest on a mortgage, has surprisingly decreased over a period of decades. In 1984, 38% of the median homeowner’s paycheck went to paying the median mortgage. That portion decreased to 31.5% in 2024. Strangely, this runs counter to the narrative about the increasing cost of home ownership.

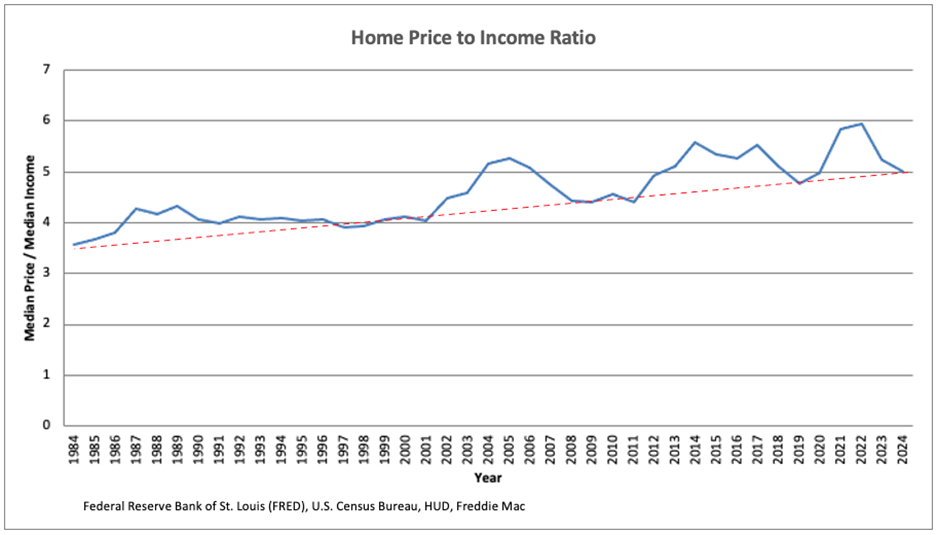

But let’s look at it from another angle. The ratio of median home price to median household income has increased over that same period. In 1984, the median price of a home was about 3.5 times the size of the median homeowner’s paycheck. That ratio increased to just over 5 times the home price vs income in 2024, hitting a peak of 6X income in 2022.

What Does This Mean? Beyond the surface of the declining mortgage burden is the fact that this improvement was largely driven by falling interest rates, not by home prices staying in line with income. In fact, the home price to income ratio tells a different story: homes have become structurally less affordable for forty years making homebuyers heavily interest rate dependent. The increases in mortgage rates in early 2022, illustrate that point. Rates increased and mortgage burden popped from 24% to over 35% in a matter of months, like touching a hair trigger.

Taking this further, assuming the same percent down payment in 1984 and 2024 (e.g., 10% or 20%), the rising multiple of home price to income makes saving for a downpayment even harder, especially given all of the additional expenses households have competing for that money today that didn’t exist in 1984 (e.g., TV subscriptions, internet service, security systems, technology hardware and software, etc.).

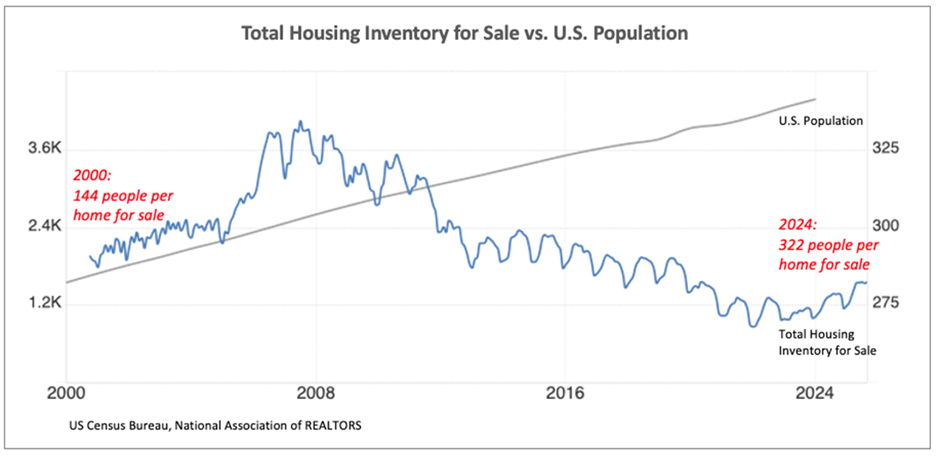

Signal 5. Housing Supply for Sale Has Tightened Relative to Population. One of the big drivers of price increases is strong demand, which in the case of homes, has been dampened by higher mortgage rates. The other big driver of price increases is tight supply which is at play in the housing market.

On the supply line alone (shown in blue) the total US housing inventory for sale has declined from a peak of just over 4,000,000 in July of 2007 (just before the 2008 financial crisis) to just over 1,000,000 in 2024, a 75% decrease. That would be a huge drop in supply even if the number of potential buyers remained constant. However, the U.S. population has grown from about 282M in 2000 to 341M in 2024 (shown in gray), and potential buyers along with it, further tightening available inventory for both existing and new homes that include single-family houses, condominiums, and co-ops.

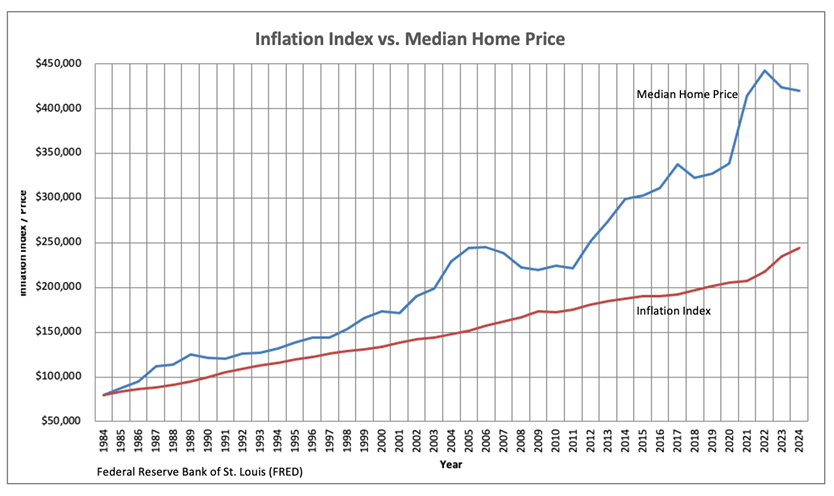

What Does This Mean? Supply of housing inventory for sale per person has tightened by more than 220% from 144 people per home for sale in 2000 to 322 people per home for sale in 2024. This dramatic tightening of supply has been a major contributor to the increase in home prices and the increase in home price to income ratio we saw earlier, which has outpaced income growth. As we can see below, median home price has outpaced inflation with its largest jump after 2011. Tightening of home supply may be a major factor driving this increase.

Signal 6. The “Cheaper to Rent Than Buy” Myth May be Clouding the Understanding of Would-Be Buyers. The media has recently parroted the “cheaper to rent than buy” message, which is great for their provocative headlines, especially considering all the signals we reviewed above. But the cheaper to rent argument assumes that people look at costs and benefits only monthly, again luring would-be buyers into the “life-as-a-service” trap.

What Does This Mean? While it’s true that in many markets, monthly rent is less than a monthly mortgage payment at current prices and interest rates, the monthly cost assumption does not consider the non-monthly financial benefits of home ownership, even at a higher monthly cost. These benefits include the facts that part of the monthly payment goes toward equity, mortgage interest and property taxes are often tax deductible at year-end, the real estate asset has a high likelihood of appreciating over a period of years, and equity can be leveraged at a lower rate than consumer credit. But, if would-be buyers only look at housing as a monthly service cost, they may never access these benefits.

What Does This Mean for Profitable Revenue Growth?

Now that we know some of the big signals around the housing market and the risks of life-as-a service for the next generation,

- The 50-Year Mortgage is Not a Panacea for Home Ownership Affordability.

- First-Time Home Buyers Are Showing Up Late to the Mortgage Burning Party.

- Mortgage Rates Have Increased but Are Low in Historical Context.

- Home Ownership Affordability Has Become More Interest Rate Dependent Than Price Dependent Over Time.

- Housing Supply for Sale Has Tightened Relative to Population.

- The “Cheaper to Rent Than Buy” Myth May be Clouding the Understanding of Would-Be Buyers.

Let’s look at some of the dynamics and how your organization may address the needs of your customers in the homebuyer market or your customers that serve these end customer homebuyers.

Different Motivators – Homeowners vs. Landlords. For the same asset (house, townhouse, or condo) the economic motivators are very different and contribute to the economy in different ways.

Landlord and Investor Motivations. Homes have been a longtime staple for real estate investors, and they bring a valuable product to the market for renters, many of whom are stepping toward homeownership. Landlord and investor motivations are primarily to maximize Net Operating Income which means:

- Maximizing rental revenue with the highest price the market will bear.

- Minimizing operating expenses by not spending or shifting costs like maintenance to the tenant.

- Investing only what’s required to market the property, keep tenant satisfaction up, and meet local regulations.

Homeowner Motivations.Homeowners, on the other hand, have a very different set of motivators. In most cases, their motivators are to maximize quality of life and utilization of the home. Rather than looking at Net Operation Income, like an investor, they’re spending in other ways that are attached to the property. These include:

- Investing in home improvements and discretionary upgrades to improve livability and home value.

- Maintaining the property, often beyond what a landlord would in a rental home.

- Spending on outdoor improvements like hardscaping and landscaping. This is a no-man’s land for who will pay the bill in rental houses.

- Leveraging home equity lines of credit to fund it all which would be non-existent in a rental home.

Homeownership is foundational for driving the economy and the trends we reviewed can lead us on a long-term precarious path for the next generation. While the investor service of transitioning tenants to eventual homeownership is valuable, a decline in homeownership is not good for economic health. If the mix shifts toward rentals, spending will likely shift away from discretionary upgrades to maintenance minimums, slowing demand for higher end home goods and furnishings, renovation services, and building products.

Weakening the Equity Engine. Life-as-a-service weakens the equity engine that fuels the economy through less discretionary spending funded by home equity lines, less collateral for other real estate investments or starting new businesses, and less capacity to absorb family financial events like medical costs, job layoffs, and college tuition that’s not covered by savings. And later in life, many seniors are turning to equity built over the years to fund their retirement and enable them to age-in-place in their family home rather than moving to a senior living community. None of this would be possible in the future in a life-as a service model.

How Might You Help Your Customers?

If you serve markets that depend on homeowners such as financial services, home goods, furnishings, home services, building materials, and real estate, you have opportunities.

1. Improve Entry Points and Flexibility for Homeownership. If you’re in finance, housing, or related services:

- Design products that help renters build credit and qualify sooner and become homeowners earlier in life with loan durations that allow them to enjoy the benefits of the equity they build.

- Create offers that align with new homeowner mobility and allow them to take their mortgages with them. Portable mortgages (now used in Canada, the U.K., Europe, and Australia) give the homeowner the ability to move their mortgage to the next property, adjusting the balance based on the price, while maintaining the interest rate and term. Since the average homeowner lives in their home for about 12 years (less for first time buyers), portability gives them more flexibility and can also open up inventory of owners unwilling to sell and lose their current low interest rates.

- Explore rent-to-own structures or shared-equity models that get households on the ladder without a traditional 20% down payment.

- Build long-horizon down-payment accumulation products with automated contributions and matching incentives from employers or partners. If you’re in financial services, instead of rounding up the credit card purchase to the next dollar, round it to the next ten or twenty. Then create an extra incentive to pay the credit card bill in full monthly to avoid interest charges. You may lose some short-term interest in the interest of capturing new customers early in their careers with a huge lifetime value.

2. Make Ownership Operations More Affordable. Opportunities abound across sectors:

- Financial Services: Develop home-equity products that are transparent, responsibly underwritten, and easy to manage digitally to make them simple to use for home operations.

- Home Goods and Furnishings: Offer modular, upgradeable solutions that fit smaller spaces now and scale later with the first home purchase. Create financing options that don’t trap customers in revolving debt but make them customers through each stage of home ownership.

- Home Services and Utilities: Help customers manage their total cost of occupancy with maintenance plans and bundled services that flatten surprises rather than spike them.

3. Serve the Investor and Landlord Side of the Asset. Investors own about 20% of the 86M single family homes in the United States with small and mid-sized investors owning 85% to 90% and institutional investors owning the remaining 10% to 15% of the total investor share. As investor ownership continues to grow due to opportunities from worsening homeowner affordability, you may consider opportunities to:

- Create offers specifically for small and mid-sized investors to make property acquisition easier including ready lines-of-credit, faster closings, smoother diligence periods, ready-to-go insurance, renovation services without contractor hassles, and predesigned tenant marketing and brokerage packages.

- Develop services for landlords and professional property managers to make managing easier including maintenance and management services, property monitoring, property management technology, and tenant experience offers.

- Segment your messaging and offers for investors and landlords to address their priorities around risk, speed, and operating income creation.

Ten Questions About Your Customer Strategy for the Housing Market. To set your direction, here are ten questions you may ask your organization:

- Where does our growth today depend, directly or indirectly, on homeownership levels in our core markets?

- How exposed is our revenue to a continued shift from owner-occupied homes toward rentals or institutional ownership?

- What specific customer segments (first-time buyers, move-up buyers, small landlords, institutional landlords) are untapped potential for us?

- If the median first-time buyer age stays consistent or increases, how does that change the timing and nature of demand for our products and services?

- What would a “housing-as-a-service” world mean for our offers and could we create subscription or usage-based models that fit monthly cash-flow thinking?

- Where could we partner across finance, real estate, home services, and home products to lower the friction of getting into a first home or staying in one?

- If the housing market is an opportunity for us, how will we monitor the key Signals and who in our organization is accountable for acting on them?

- What assumptions about “normal” mortgage rates, cost of capital, and other housing market indicators are baked into our current three-year plan and how can we capitalize if the market shifts from those assumptions?

- How can we help our business-to-business customers translate today’s housing environment into their own growth strategies that may involve our offers?

- If a 50-year mortgage becomes common in our markets, what new offers, like bundled life services would we build to align with a life-as-a service customer?

Your Call to Action Each of the questions that apply to your organization should prompt valuable conversation and ideas around your business and your customer strategy for the housing market. Homeownership has been one of the quiet engines of the U.S. economy fueling spending, entrepreneurship, and wealth creation for generations. The Signals we’re seeing now suggest that engine is under strain, especially for younger households.

Look at each of the signals we’ve discussed around home prices, rates, affordability, homeownership, and buyer age. Then, consider their impact from two perspectives: How will they affect your customers and their ability to grow? How will they affect your business?

Get beyond current state and ask your team where they see the signals projecting ahead and what this means for your organization's profitable growth. Consider each of the questions I've asked, add your own, create a plan, and get into action. Questions for us? Email us at info@salesglobe.com or contact us at SalesGlobe.com.

SalesGlobe is a revenue growth consulting and services firm focused on helping our clients reach their growth aspirations through better solution development and operationalizing to get results.

Mark Donnolo is the author of SalesGlobe Signals with research assistance for this issue from Nabeel Saleheen.

*When did the 30-year mortgage begin? It seems like a fixture today but it’s relatively new, starting after the Great Depression of the 1930s. Before the 1930s, loan terms were typically 5 to 10 years, with 40% to 50% down payments and had little or no amortization. Payments primarily covered interest, and the entire principal was due in a balloon payment at the end of the short term, requiring continuous refinancing by the few families who owned homes. After the mortgage crisis of the 1930s, and hundreds of thousands of foreclosures, the Federal Housing Administration (FHA) was created to establish a stable, national mortgage market with standards that set a maximum loan term of 20 years with a minimum down payment of 20%. After World War II, The FHA loan term was extended to 30 years. The 30-year fixed-rate mortgage resulted in a dramatic surge in ownership with the US homeownership rate rising from about 44% in 1940 to almost 62% by 1960. That rate sits at about 65% today. This growth established homeownership as a pillar of the American middle class and a foundational driver of the economy.

Founder and Managing Partner at SalesGlobe

“We help companies solve tough sales challenges to connect their sales strategies to the bottom line.”

{kind=link}

{kind=link}

{kind=link}