The Great Generational Wealth Transfer Will The Kids Save It or Spend It?

The Great Generational Wealth Transfer

Will The Kids Save It or Spend It?

What You Need to Know

- ◆Baby Boomers, one-fifth of the population, control half of U.S. household wealth.

- ◆That concentration is moving with nearly $100 trillion in wealth transfers through 2048 from Boomers and older at a rate of $1 trillion per year.

- ◆The first Baby Boomers turned 80 in January 2026, and deaths are projected to reach 4 million per year by 2037. The bulk of estate transfers is still ahead.

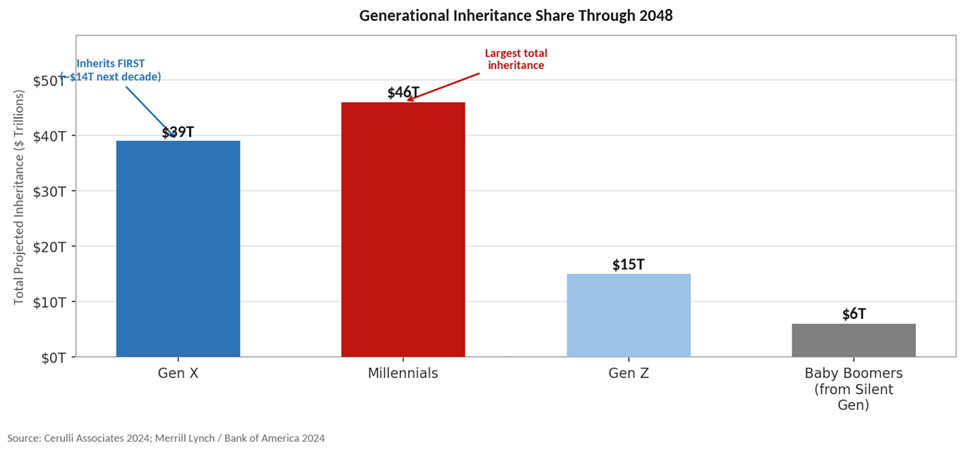

- ◆Transfers will cascade with Gen X first ($14 trillion over the next decade), Millennials inheriting the most ($46 trillion by 2048) followed by Gen Z ($15 trillion).

- ◆Wealth is concentrated with 2% of households accounting for 50% of all transfers. Most Americans will inherit far less than headlines suggest.

- ◆Younger inheritors plan to invest and pay down debt first and spending priorities will differ from Boomers.

- ◆72% of millennial and Gen Z investors don’t believe in traditional investments.

- ◆For wealth management and financial firms, the largest risk is not a market downturn. It is the younger beneficiary they’ve never met and the relationship they’ve never established or developed.

SalesGlobe Signals is about seeing a bigger, macro view on growth and taking actions that will help you reach your growth aspirations. This month let's look at the Signals around the greatest intergenerational wealth transfer in American history… the Great Generational Wealth Transfer.

In Signals, our focus is on helping executives answer two questions for their businesses:

- What Are the Market Signals? Indicators you might watch for your business that may signal what's ahead.

- What Does This Mean for Profitable Revenue Growth? Based on the signals, how you may think about growth and the actions you may consider.

What Are the Market Signals?

The largest private wealth transfer in American history is not a future event. It is happening now, and it will reshape every industry that serves, advises, or sells to American households.

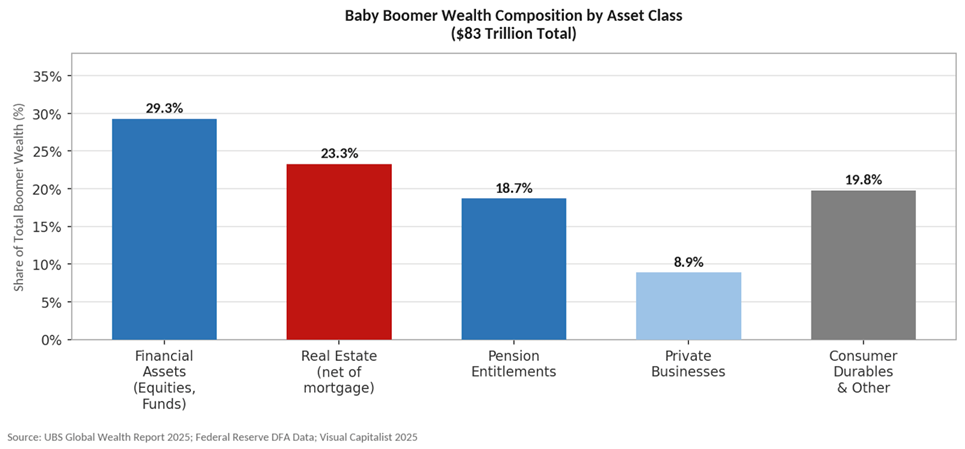

Baby Boomers were born into a world of postwar optimism and exited the workforce owning more than half of everything Americans possess. They caught tailwind after tailwind: a rising stock market that delivered a fourfold surge during their peak earning years, homeownership that was accessible and subsidized, defined-benefit pensions, and decades of falling interest rates that inflated asset values year after year. The result is a generation that now controls more than $83 trillion in household wealth, more than ten times what Millennials hold today.

That wealth is not staying put. The transfer from Boomers and the older Silent Generation to Gen X, Millennials, and Gen Z is moving at roughly $1 trillion per year in bequests and living gifts. And it will accelerate dramatically. On January 1, 2026, the leading edge of the Baby Boom reached age 80. Boomer deaths are expected to climb from 2.6 million per year today to 4 million annually by 2037, with the peak arriving in the mid-2040s. What looks like a slow trickle today will become a flood over the next two decades.

The questions that matter for business leaders are not just demographic. They are strategic. Who gets the money? When do they get it? What form does it arrive in? What will they do with it? And which industries stand to win or lose as trillions of dollars change hands? Let’s look at the Signals.

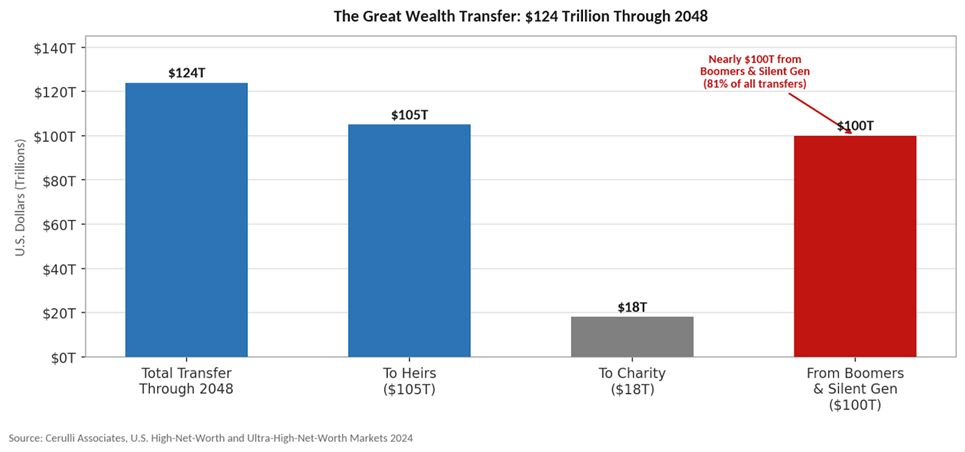

Signal 1. The Transfer’s Scale Is Unprecedented: $124 Trillion Through 2048.

Numbers this large cannot be ignored. $124 trillion will change hands in the United States through 2048*. Of that total, $105 trillion will flow to heirs and $18 trillion to charitable organizations. To put the heir figure in perspective, U.S. GDP in 2023 was approximately $27 trillion. So, the wealth being transferred to the next generation is nearly four times the annual output of the entire American economy.

The transfer is already underway. Both the Baby Boomer (born from 1946 to 1964) and Silent Generation (born from 1928 to 1945) cohorts together control an estimated $105 trillion, and roughly 0.6% of all U.S. household wealth is changing hands through inheritance or gifts every single year. Required minimum distributions from tax-deferred retirement accounts are pumping hundreds of billions of dollars into senior spending annually that are going to wealth transfer, investments, and consumer spending. These flows are legally mandated and trending higher as more Boomers enter their 70s. The giving is also happening voluntarily. Nearly half of first-time homebuyers now receive parental gifts for down payments, often $20,000 to $50,000 at a time. Looking back at the challenges for first time home buyers in previous SalesGlobe Signals issues, these gifts are helping to ease the difficulty of coming up with large down payments.

The wealth transfer is not a future scenario to plan for someday. Wealth is already moving, and your business model may need to start moving as well if it depends upon asset flows and spending that may come from this transfer.

What Does This Mean for Profitable Revenue Growth? For companies across virtually every sector, the Great Wealth Transfer is the largest demand-side event in a generation, not because it creates new needs, but because it supercharges existing ones and accelerates them across demographic groups that have been underserved or undercapitalized. Financial services firms (wealth managers, investment advisors, trust companies, estate attorneys, and tax professionals) are sitting at the center of this event. The question for firms in those spaces is not whether growth will come, but whether they will capture it.

The challenge is that advisors risk losing assets at the point of transfer. Studies show that only 19% of younger inheritors continue with their parents' financial advisor. For wealth management firms, the largest risk is not a market downturn. It is the beneficiary they’ve never met and the relationship they’ve never established or developed. Companies that invest now in multigenerational relationship models, through family meetings, digital engagement tools, and estate planning discussions, will be best positioned to retain assets as they move.

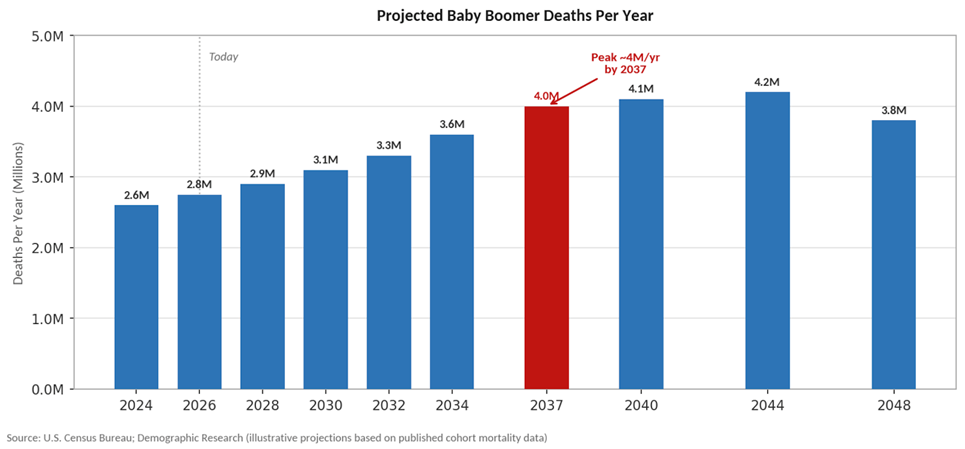

Signal 2. The Oldest Baby Boomers Turned 80 This Year. The Clock Is Running.

On January 1, 2026, the oldest Baby Boomers crossed into their ninth decade. Born between 1946 and 1964, Boomers range in age from 62 to 80 today, and by 2030 the youngest among them will be 66. The death rate within the cohort is already accelerating. Approximately 2.6 million Baby Boomers die each year today, a figure projected to approach 4 million annually by 2037. By the mid-2040s, roughly half the Baby Boomer population may be gone.

The timing matters because inheritance is not evenly distributed across the calendar. Most Boomer wealth is still attached to living individuals. The big wave of estate transfers is coming in the 2030s and 2040s, but the planning decisions, relationship-building, and strategic positioning need to happen now. Boomers entering their 80s are also beginning to make healthcare and long-term care expenditures that will erode some of that wealth before it transfers. The median annual cost of a private nursing home room exceeded $108,000 in 2021, and costs continue to rise. For many families, healthcare spending will be the single largest variable affecting how much actually passes to heirs.

There is an important nuance here: the transfer does not wait for death. The “give while you live” ethos is increasingly popular among affluent Boomers. Many are helping adult children buy homes, pay tuition, or fund businesses now, turning portfolio wealth into immediate consumption well ahead of their own passing. This means the demand effects of generational wealth transfer are already present in the economy.

What Does This Mean for Profitable Revenue Growth? Industries serving the elderly, including healthcare, home care, assisted living, hospice, and medical devices, face enormous near-term demand as the Boomer cohort ages. The longevity economy already generates an estimated $8.7 trillion in global spending annually, projected to reach $15 trillion by 2030. For health systems, pharmaceutical companies, and long-term care operators, Boomers remain the dominant revenue driver for at least another decade.

For estate planning attorneys, CPAs, and financial advisors, the window to position for Boomer wealth planning is narrowing. The clients who need trust structures, Medicaid planning, charitable vehicles, and estate tax strategies are alive today. The firms that establish those relationships now capture both the planning work and the post-transfer asset management. Those who wait will find they are competing for the attention of inheritors who already have advisors and other loyalties. Financial advisor business development follows the same patterns that business development follows in industries like technology, healthcare, and business services. Everybody sells and the financial advisory business is no exception.

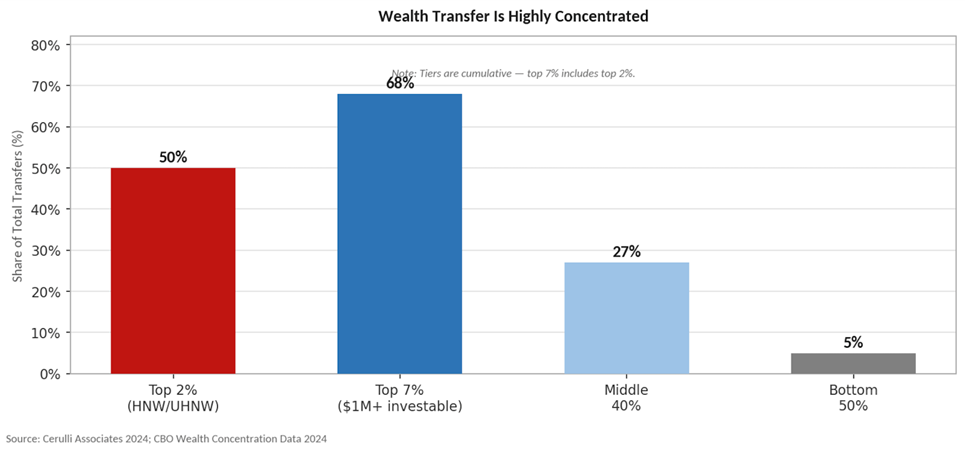

Signal 3. The Wealth Is Concentrated and So Are the Opportunities.

The headline numbers on the Great Wealth Transfer are massive, but they can be misleading without context. The distribution of wealth being transferred is deeply unequal. 2% of U.S. households, those classified as high-net-worth or ultra-high-net-worth, will account for approximately 50% of all transfers, roughly $62 trillion according to Cerulli Associates. The top 6.9% of households, those with at least $1 million in investable assets, are projected to account for 68% of total wealth transferred.

At the other end of the spectrum, the bottom 50% of Boomer and Silent Generation households will pass down approximately $6 trillion collectively. Most Americans may receive little or nothing. A Northwestern Mutual study found that only one-third of Millennials expect to receive an inheritance, while only 22% of Boomers plan to leave one, leaving a gap in expectations. Some Boomers will spend much of their wealth in retirement, face healthcare costs that erode their estates, or outlive the assets they expected to pass down. As I described in our SalesGlobe Signals issue on Where Have All the Babies Gone?, there is a real financial cost to increasing longevity. The gap between what younger generations expect to inherit and what they will receive is a meaningful planning risk.

Geography adds another layer. Boomer wealth is concentrated in coastal markets, major metros, and Sun Belt retirement destinations. In Florida alone, retirees 65 and older make up more than 50% of homeowners in cities like North Port, Naples, and Cape Coral. In the North Port-Bradenton metro, retirees own an estimated $97 billion in real estate. Firms with a geographic strategy tied to retirement concentration zones will see disproportionate opportunity.

What Does This Mean for Profitable Revenue Growth? For financial services, insurance, and professional services firms, this data makes clear that the highest-value opportunity is not mass market. It is the affluent and high-net-worth segment. The 1.2 million individuals with net worth above $5 million are projected to pass down more than $38 trillion over the next decade. These clients need sophisticated estate planning, trust services, family governance frameworks, and tax optimization strategies that go well beyond a standard financial plan.

Real estate developers, luxury retailers, and wealth-adjacent consumer businesses should consider geographic concentration strategies. Markets with high retiree density, like coastal Florida, Sun Belt metros, and affluent suburban areas in the Northeast, are not just retirement markets. They are inheritance origin markets, and the communities where heirs will return or sell property into will be shaped by where the wealth currently sits. National and local businesses that understand this dynamic can position services and products to provide value to this market.

For consumer goods and services companies that serve mass market audiences, the key insight is to focus on the mighty middle segments, the portion of the population that will receive modest but meaningful inheritances and make behavioral changes at the margin. Even a $50,000 inheritance can accelerate a home purchase, fund a business, or generate a decade of new investment activity.

Signal 4. The Wealth Being Transferred Is Dominated by Real Estate and Equities, Two Asset Classes with Very Different Transfer Dynamics.

Baby Boomers built their wealth primarily through two channels: the stock market and real estate. Financial assets (equities, mutual funds, and pension entitlements) represent the largest single component of Boomer wealth, at roughly 29% of their total holdings. Real estate, net of mortgage debt, represents another 23%. Together, these two asset classes account for more than half of what is being transferred.

The form of wealth matters because it determines how and when transfer occurs, and what happens next. Equities and liquid financial assets pass relatively cleanly through estates. They can be sold, diversified, or invested according to heir’s preferences within months of a transfer. Real estate is far more complicated. Heirs often live far from inherited properties, face capital gains implications, carry costs, or simply prefer cash over management responsibility. A Coldwell Banker study estimates $2.4 trillion in U.S. real estate will change hands over the next decade among affluent households, with many heirs expected to sell rather than retain inherited properties. That produces cash that must be reinvested, often into financial assets.

Pension entitlements represent another major component. Nearly $20 trillion sits in tax-deferred retirement accounts held by Baby Boomers and the Silent Generation. Required minimum distributions already pump hundreds of billions into senior spending annually, and inherited IRAs pass specific rules about distribution timelines to non-spouse beneficiaries, meaning that inherited retirement assets often flow into consumption or reinvestment quickly after transfer.

What Does This Mean for Profitable Revenue Growth? Real estate professionals (brokers, agents, developers, and property managers) face a wave of inventory that will eventually be released from the aging Baby Boomer cohort. Today, many Baby Boomers are choosing not to sell. National Association of Realtors data shows only 21% of Baby Boomer respondents said they wanted to pass assets to the next generation while they’re still alive. That hesitancy will shift as health declines and estate planning becomes urgent. When it does, the release of a decade's worth of pent-up Baby Boomer property inventory will reshape local housing markets in retirement destination communities.

For financial institutions managing inherited assets, the influx of new clients with investable assets creates both an opportunity and a service model challenge. Heirs inheriting a mix of real estate, securities, and retirement accounts need integrated advice across estate taxes, asset liquidation timing, portfolio construction, and real estate disposition. The institutions that can offer a holistic solution, rather than siloing investment management, mortgage banking, and trust services, will capture disproportionate wallet share.

Insurance companies should pay close attention to the real estate transfer dynamic. Inheritors who sell properties often have proceeds available for reinvestment, and many will seek income-generating alternatives. Annuity products, life insurance-based wealth vehicles, and whole life policies can all be positioned to capture assets that are newly liquid and seeking structure.

Signal 5. Who Receives the Wealth, and When, Determines Everything.

Gen X receives first. Despite being perpetually overlooked between the massive Baby Boomer and Millennial cohorts, Gen X, now approximately 45 to 61, will inherit an estimated $14 trillion over the next decade, more than any other generational cohort in that timeframe. For many Gen Xers, this is a pivotal moment because they are simultaneously sandwiched between aging parents and adult children, carrying the costs of both. They lost 38% of their median net worth in the 2008 financial crisis, which is a deeper hit than any other generation, and have been understandably pragmatic about money ever since. An inheritance that arrives in their 50s lands at a moment when retirement is impending and planning decisions are urgent.

Millennials, born between 1981 and 1996 and now between ages 30 and 45, will ultimately inherit the most of any generation: $46 trillion by 2048. They have faced a uniquely difficult accumulation environment—$1.5 trillion in collective student debt, two recessions before age 40, and a housing market where median prices rose more than 400% between 1990 and 2024 while incomes lagged. For Millennials, an inheritance is not just a windfall; for many it represents the first real foothold in an asset-building system that has been difficult to enter.

Gen Z, born 1997 and after, will receive $15 trillion. Their spending is already rising fast, projected to reach $12.6 trillion globally by 2030, and their inheritance, while smaller in absolute terms, will arrive during their prime earning and investing years. Gen Z investors started earlier. The average Gen Z investor made their first investment at age 20, compared to 31 for Baby Boomers.

What Does This Mean for Profitable Revenue Growth? The generational sequencing of inheritance creates a segmented opportunity landscape. For the next decade, Gen X is the primary inheritor, and Gen X behaves differently from Millennials. They are more risk-averse, more likely to work with established financial institutions, and more focused on retirement security than impact investing. They also have more immediate financial pressure. Companies that serve the Gen X group in their 50s should expect that customers they have known for years will suddenly have substantially more assets and different needs.

Millennials, as the eventual largest inheritor cohort, are the long-term prize for financial services, real estate, and consumer companies. But they are also the generation most likely to change advisors, seek digital-first service models, and demand that their wealth be managed in alignment with their values. Companies building for the Millennial inheritor segment need to invest now in digital capabilities, sustainability-aligned products, and transparent pricing models.

Gender matters too. Women will be inheritors in disproportionate numbers, as wives statistically outlive husbands and inherit first within a household before assets pass to children. Cerulli estimates $54 trillion will move horizontally to widowed women before flowing to the next generation. Financial services companies that have historically designed products and experiences around male clients face a meaningful gap that the Great Wealth Transfer will expose.

Signal 6. Will They Spend It or Save It? Inheritors Are Planning to Invest, With Different Values.

Every company with a stake in consumer spending or capital markets should be asking the behavioral question. When the money arrives, what happens next? The beneficiary generations will act differently than prior generations.

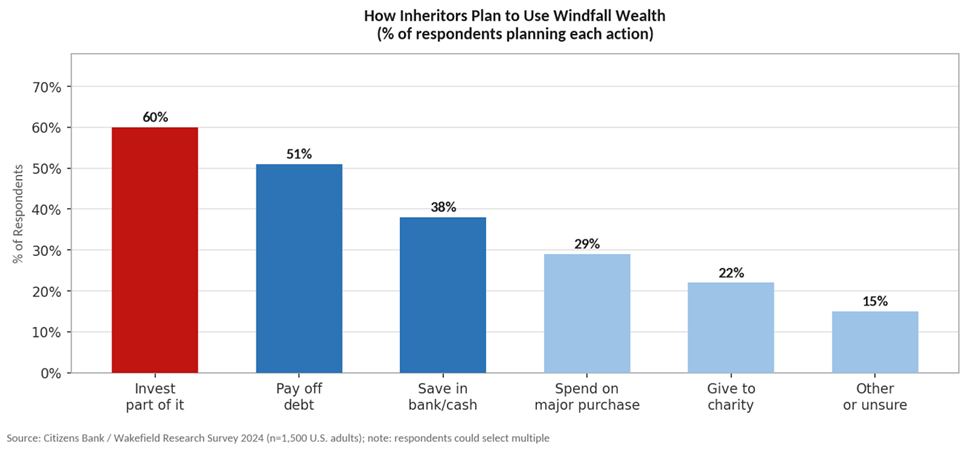

The early evidence is more reassuring for investors than for consumer spending companies. A Citizens Bank survey of 1,500 Americans found that 60% of inheritors plan to invest part of any windfall, while 51% plan to use inheritance to pay off debt. They are not prioritizing consumption, by purchasing that new car or going on that big international vacation. At least initially, inherited wealth appears more likely to enter investment and debt repayment channels than consumer spending.

But values-based investment differences, among some segments, will reshape capital markets over time. Some 72% of millennial and Gen Z wealthy investors surveyed by Bank of America believe it is no longer possible to achieve above-average returns solely through traditional stocks and bonds. They are more open to private equity, direct investments, impact funds, and alternative assets. ESG considerations influence 82% of respondents between ages 24 and 43 when making investment decisions, compared to just 41% of all respondents, although having a double bottom line (e.g., ESG and profit) has been shown to lower overall investment returns. As this cohort's assets under management grow, the direction of capital will shift.

There is a complicating wildcard, however: long-term care costs. The median annual cost of a private nursing home room now exceeds $108,000. For the many Baby Boomers who will spend years in some form of assisted living or home care, a significant portion of the projected transfer wealth will be consumed before it ever reaches an heir. And the heirs themselves increasingly expect to bear some of those costs. 53% of Millennials and Gen Z say they expect to be financially responsible for aging parents, and 52% say that expectation is already affecting their own financial planning.

What Does This Mean for Profitable Revenue Growth? For investment managers, asset managers, and fintech companies, the coming decade represents a customer acquisition window unlike anything since the 401(k) revolution. Trillions of dollars will arrive in the hands of people who are not yet deeply engaged with any institution and who have different preferences from the parents whose assets they are inheriting. Firms that lead with digital-first onboarding, transparent fees, alternative asset access, and purpose-driven investment options will be positioned to capture these flows. Firms that rely on legacy models risk being bypassed entirely.

For consumer companies, including durables, retail, automotive, luxury, travel, the outlook is more nuanced. Debt repayment and investment will absorb a significant portion of inherited wealth, particularly for Millennials burdened with student loans. But the marginal impact of financial relief on spending behavior is real. Millennials who inherit enough to pay off student loans or make a home down payment will free up monthly cash flow that cascades into broader consumer spending over years. The consumer spending effect of the transfer is not immediate. It is a 5-to-10-year tailwind that will grow as the transfer accelerates.

Banks and consumer financial institutions should be watching deposit flows carefully. As inherited assets arrive (cash from liquidated real estate, proceeds from brokerage transfers, checks from estate administrators) they will pass through checking and savings accounts before being allocated. The bank that holds those assets in the 90-day period after a transfer and before reallocation has the highest conversion opportunity. Proactive outreach and wealth onboarding programs tied to estate settlement events are among the highest-return investments a retail bank can make.

Ten Questions About Your Growth Strategy on the Great Generational Wealth Transfer

To set your direction, here are ten questions you may ask your organization:

- What is our current exposure to the Baby Boomer wealth holder segment and what share of that business will move to heirs in the next five years?

- Have we identified the next-generation clients within our existing customer relationships? Do we have any contact with the children or spouses of our current clients?

- What percentage of our revenue today serves the affluent and high-net-worth segment where the majority of wealth transfer value is concentrated?

- Is our service model designed for the preferences of Gen X and Millennial inheritors (e.g., digital access, transparent pricing, ESG alignment, and integrated financial planning)?

- How will our business perform if the first wave of Baby Boomer real estate is released to the market in our geographic areas? Are we positioned to serve sellers, buyers, or both?

- For companies in financial services: What is our plan to retain assets when a primary client passes? Do we have relationships with the beneficiaries, and have we conducted any multigenerational family planning meetings?

- What does the evidence tell us about how our target customers will use inherited wealth? Will they spend it with us, invest it elsewhere, or use it to pay down debt? How does our growth strategy account for each scenario?

- Are we positioned in the geographic markets where Baby Boomer wealth is most concentrated, such as coastal Florida, Sun Belt metros, and affluent Northeast suburbs, and do we understand the local wealth transfer dynamics in those markets?

- What is the role of women in our customer strategy? Given that $54 trillion will transfer horizontally to widowed women before reaching the next generation, are our products, services, and relationships designed with women as primary clients?

- What is our 10-year scenario for this category? If $46 trillion moves to Millennials by 2048, and Millennials behave differently from their parents as consumers and investors, what does our business look like at the end of that transfer?

Your Call to Action

The Great Generational Wealth Transfer is the single largest redistribution of private assets in American history. It is not a trend to watch. It is a structural shift already reshaping financial markets, consumer behavior, real estate dynamics, and the competitive landscape for every industry that serves American households.

Consider these Signals from two perspectives: How will they affect your customers and their ability to grow? And how will they affect your own business, your customer and client base, your product mix, your distribution model, and your competitive positioning?

Get beyond current state and ask your team where they see the signals projecting ahead and what this means for your organization's profitable growth. Consider each of the questions I've asked, add your own, create a plan, and get into action.

We would enjoy a conversation about what this means for your business and your growth strategy. Reach out at info@salesglobe.com or visit us at SalesGlobe.com.

SalesGlobe is a revenue growth consulting and services firm focused on helping our clients reach their growth aspirations through better solution development and operationalizing to get results in sales strategy, go-to-market, account strategy, and sales compensation.

Founder and Managing Partner at SalesGlobe

“We help companies solve tough sales challenges to connect their sales strategies to the bottom line.”

{kind=link}

{kind=link}

{kind=link}