Housing Affordability? It’s About Supply. What it Means for Your Revenue Growth.

Housing Affordability? It’s About Supply.

What it Means for Your Revenue Growth.

What You Need to Know

- ◆ Housing affordability is a supply problem disguised as a financing problem

- ◆Inventory per capita has tightened dramatically since 2000.

- ◆Supply growth is at the region and state level, not national and there are clear winners and losers.

- ◆Regulation is a material drag on housing starts per capita.

- ◆Institutional investors are a small share of total supply and are more of a media soundbite than a market factor.

- ◆Small and mid-sized investors are a market in themselves.

- ◆Shifts toward state level deregulation may boost supply in those markets.

- ◆New innovations like 3D printed homes may change the landscape and speed of supply creation.

SalesGlobe Signals is about seeing a bigger, macro view on growth and taking actions that will help you reach your growth aspirations. This month let’s look at some Signals on the supply side of the housing market.

In Signals, our focus is on helping executives answer two questions for their businesses:

- What Are the Market Signals? Indicators you might watch for your business that may signal what's ahead.

- What Does This Mean for Profitable Revenue Growth? Based on the signals, how you may think about growth and the actions you may consider.

What Are the Market Signals?

In an earlier SalesGlobe Signals issue, A 50 Year Mortgage? Is Next Gen Going to Live Life-as-a-Service?, we looked at some big signals on the U.S. housing market that included:

- Home prices far outpacing income growth and homeownership becoming interest rate dependent,

- The first-time buyer, now 40 years old on average, compressing the years to build equity,

- The 50-year mortgage nearly doubling total interest, and

- My assertion that “cheaper to rent than buy” is a life-as-a-service myth that endangers wealth creation.

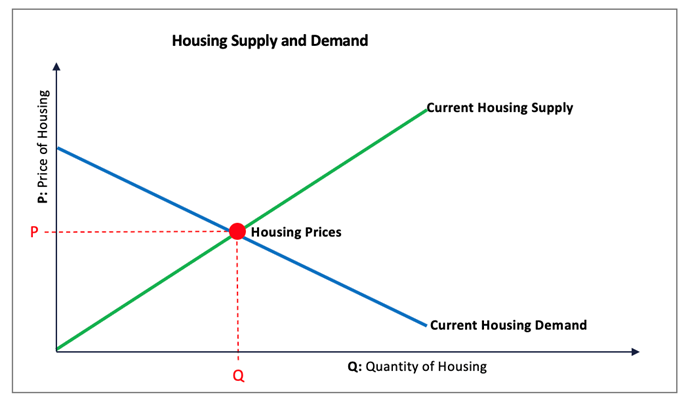

It appears that much of the homebuying attention is on the challenges first-time homebuyers have with getting into the market, with many of the solutions about lowering rates, extending loan timeframes, lowering downpayments, and other financial machinations. Reflecting upon our SalesGlobe Signals issue last year on the fundamentals of supply and demand, we know that higher home prices are the result of the intersection of constrained supply and strong demand. If housing supply holds constant (because homebuilding isn’t keeping pace with population growth or current homeowners aren’t trading up or down because they’re holding onto their low-rate post-pandemic mortgages) and housing demand remains constant, then prices will tend to remain constant.

While many of the ideas around increasing home ownership are about addressing price (through financial solutions to pay those higher prices), let’s understand that price is the result or symptom of the current levels of supply and demand.

While home affordability may be propped up in the short-run by financial mechanisms, the long-run solution, assuming demand does not decrease due to potential homeowners giving up and renting for life, will come from increased supply.

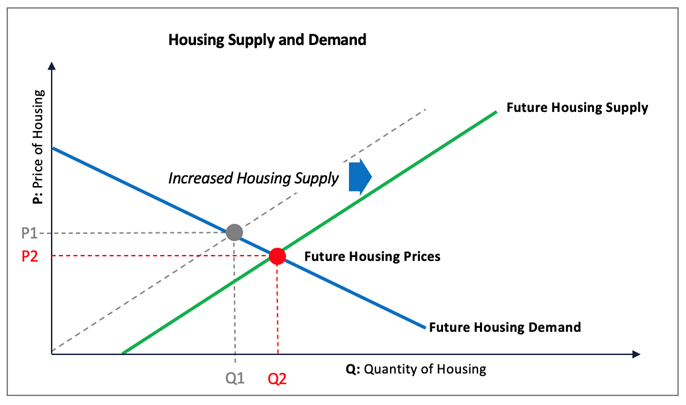

Shifting the supply curve out (the green line), while holding demand constant (the blue line), will if the fundamentals of economics hold true, decrease price (the red dot). So, in this issue, let’s focus on the supply side of the US home market, the signals around supply, and what those might mean for commercial revenue growth for your business.

Signal 1. Housing Supply has Tightened to a Multi-Decade Low Relative to Population Growth. One of the big drivers of price increases is strong demand, which in the case of homes, has been dampened by higher mortgage rates. The other big driver of price increases is tight supply which is at play in the housing market.

On the supply line alone (shown in blue) the total US housing inventory for sale has declined from a peak of just over 4,000,000 in July of 2007 (just before the 2008 financial crisis) to just over 1,000,000 in 2024, a 75% decrease. That would be a huge drop in supply even if the number of potential buyers remained constant. However, the U.S. population has grown from about 282M in 2000 to 341M in 2024 (shown in gray), and potential buyers along with it, further tightening available inventory for both existing and new homes.

What Does This Mean for Profitable Revenue Growth? Supply is the underlying driver of home affordability issues for first time buyers. Supply of housing inventory for sale per person has tightened by more than 220% from 144 people per home for sale in 2000 to 322 people per home for sale in 2024. This dramatic tightening of supply has been a major contributor to the increase in home prices.

In terms of this signal’s impact on revenue growth, if your business is in the homebuilding market, opportunity abounds to capture this pent-up demand. However, we’ll need to get more specific, as we go, about opportunities and constraints to capturing that demand such as geography, government regulation, and new technologies.

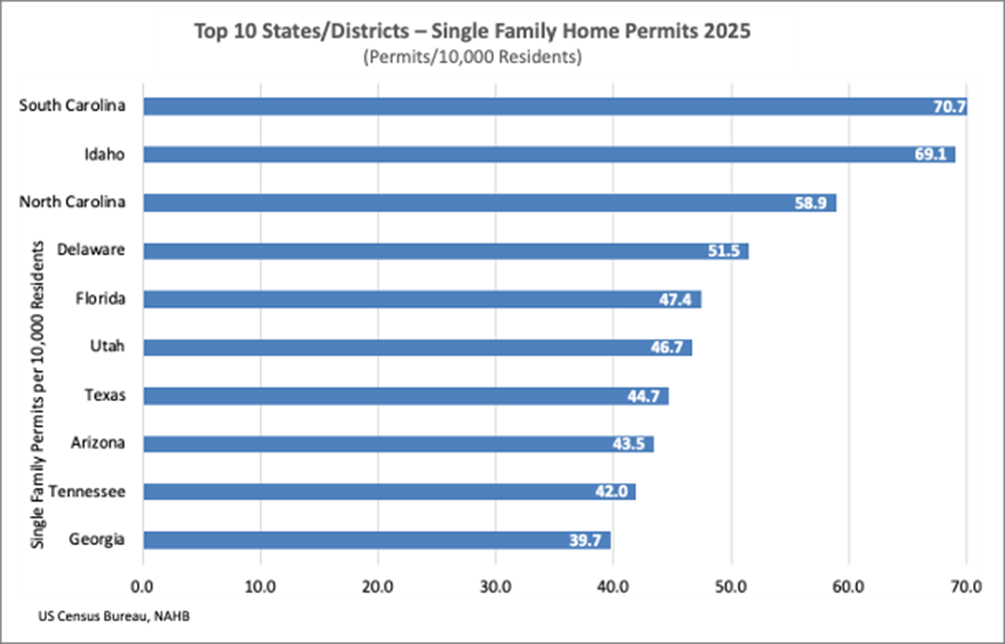

Signal 2. Housing Supply is Growing in Select Markets. While national inventory remains tight, supply growth is not uniform. Markets including the Carolinas, Idaho, Delaware, Florida, Utah, and Texas are seeing:

- Higher housing starts per capita

- Faster permit approvals

- More buildable land availability

- Lower regulatory barriers

These factors combine to make these markets fertile ground for faster housing growth as you can see in the comparative permits per capita above.

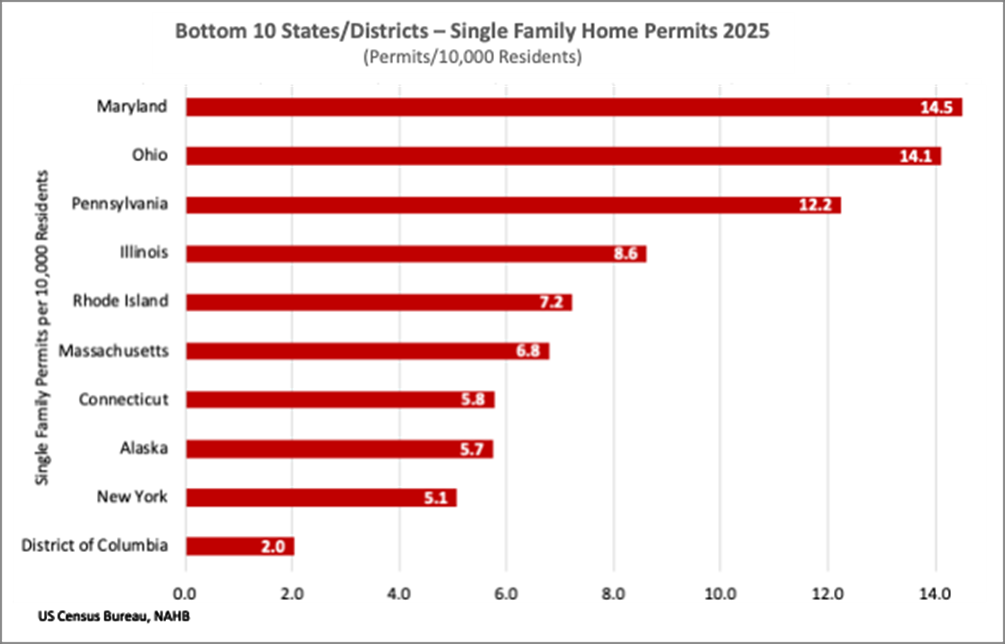

In contrast, higher-cost, higher-regulation markets like New York, Connecticut, Massachusetts, Pennsylvania, and California continue to face:

- More restrictive zoning

- Lengthier entitlement processes

- Environmental and permitting delays

- More limited developable land

What Does This Mean for Profitable Revenue Growth? In the markets that are increasing supply, there will be continued or increased homeownership in those markets as well as downstream opportunities for companies in home-related products such as financial services, insurance, home goods, furnishings, and home improvement.

If your company is in homebuilding and development, you’re likely concentrating your capital and land acquisition in faster-permitting states with less regulation. While competition in some of these high growth markets may put pressure on margins, the volume of opportunities is abundant.

If your company is in financial services, you’re likely seeing mortgage originations shift geographically, along with bank accounts, as well as underwriting standards adjusting based on the demographics and risk profile of customers in those growing markets.

If your company is in insurance, growth in the sunbelt may be increasing your exposure to catastrophe risk like hurricanes, wildfires, and flooding, all of which we’ve seen recently. Premiums have to adjust to reflect risks in those markets and states with heavy insurance underwriting regulation will continue to lose insurers.

If your company is in home goods, furnishings and home improvement, you may see growth in new households shifting demand for your offers to growing markets. And for these markets with greater homeownership, new home buyers will typically spend a couple of multiples more on these goods and furnishings than renters, which make them an attractive segment.

So, if you’re in one of these companies, you’re already experiencing these shifts in demand and, if you serve these companies, you know where you can better align with their growth.

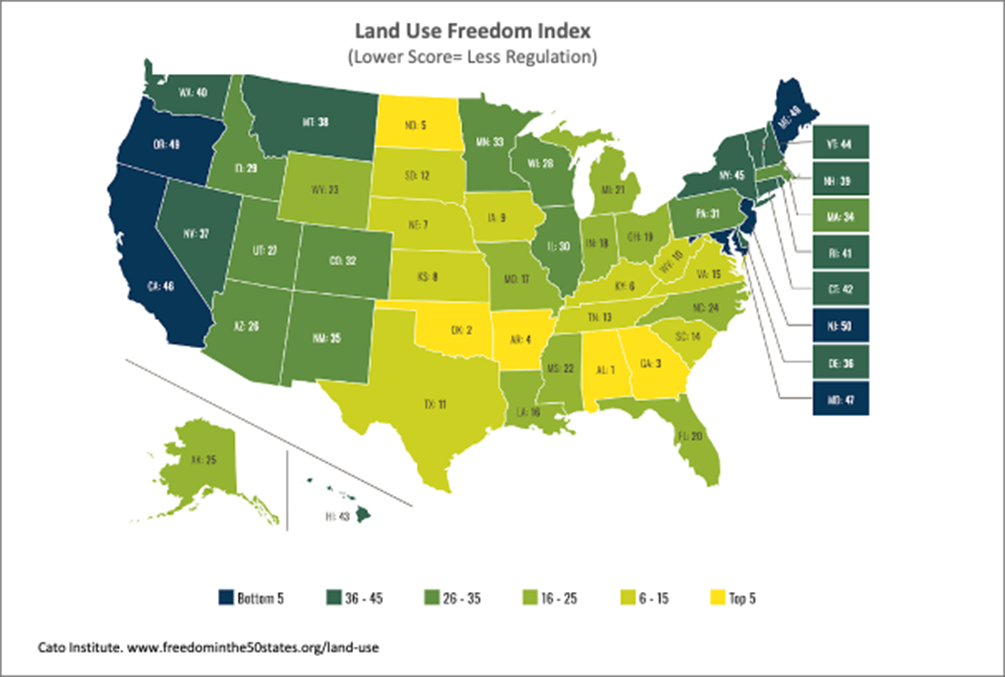

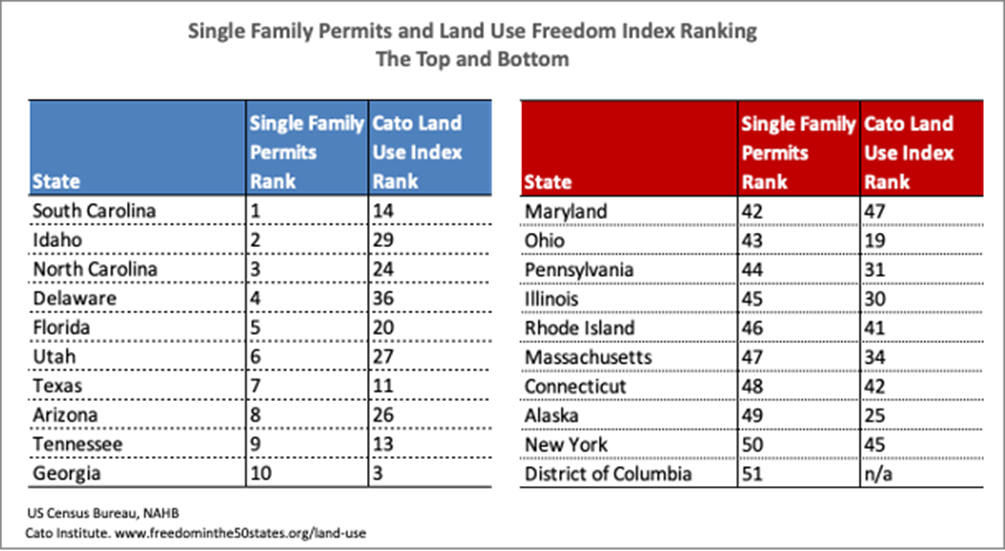

Signal 3. It’s Not the Weather, It’s the Regulation. Not surprisingly the housing supply extremes in the states above are not just due to the weather but are highly correlated with levels of state regulation that either enable or inhibit new homebuilding. The Cato Institute Land Use Freedom Index highlights states that are most and least receptive to real estate development and homebuilding. Its major variables include land use or zoning regulations and a Wharton School index to score each state. A lower score indicates greater land use freedom. Here's a look at the map and scores. Visually, the lighter shades indicate greater land use freedom.

When we look at a list of the top and bottom in terms of single family permits per capita rank, most of the top have greater land use freedom and most of the bottom have lesser land use freedom than the midpoint.

The bottom line is that high-regulation states build significantly fewer homes per capita than low-regulation states.

What Does This Mean for Profitable Revenue Growth? If your business depends on homeownership growth or you serve companies that in turn serve the homeowner market, there are two points to note. First, the high-regulation states will likely see slower unit growth, but higher prices and the low-regulation states will likely see faster unit growth and lower prices. Second, follow the path of current and future regulation. If states and municipalities lower regulation, that may indicate an opportunity to plan for greater supply growth in those markets.

Signal 4. Institutional Investors are Not a Primary Cause of National Housing Supply Constraints. Investors own about 20% of the 86M single family homes in the United States with small and mid-sized investors owning 85% to 90% of that 20% and institutional investors owning the remaining 10% to 15% of the 20% total investor share. That suggests that perhaps the media messaging about institutional investors buying up the available U.S. housing inventory, makes good headlines when in fact institutional investors own only about 3% of total single-family homes. Still, while the institutional investors may own a very small share, investor-owned housing in total, including small and mid-sized investors may meaningfully reduce entry level supply.

Given the roughly 17% small and mid-sized investor share and 3% institutional investor share, proposed federal regulations restricting institutional investor ownership of single-family homes will likely do little to impact available inventory. Government efforts might be better spent on reducing regulation as I discussed previously. And, doing anything to try to restrict small and mid-sized investor ownership would cut into the heart of our country’s free market entrepreneurialism and have more damaging implications.

What Does This Mean for Profitable Revenue Growth? The small and mid-sized investor market itself is a significant target market, depending on your offerings, and represents a larger opportunity than institutional players.

For home goods and home improvement, consider increasing focus on the small and mid-sized investor market as they may be more active renovators and upgraders than first time home buyers. They have ready capital to deploy to do the necessary work to prepare those homes for rent or resale. Oftentimes, this spending is part of the project, not discretionary. In terms of property maintenance, the same holds true broadly as owners and managers need to keep properties in marketable condition. However, in municipalities with heavy regulation like rent controls, owners have less of incentive to maintain, upgrade, or even build new properties due to limits on rental cash flow.

For financial services and insurance, consider creating offers specifically for small and mid-sized investors to make property acquisition easier including ready lines-of-credit, faster closings, smoother diligence periods, ready-to-go insurance, renovation services without contractor hassles, and predesigned tenant marketing and brokerage packages.

Across industries, consider developing services for landlords and professional property managers to make managing easier including maintenance and management services, property monitoring, property management technology, and tenant experience offers.

Segment your messaging and offers for investors and landlords to address their priorities around risk, speed, and operating income creation.

Signal 5. New Building Programs and Construction Technology May Speed Up Supply.

New Building Programs. To increase supply, there are numerous federal and state programs both proposed and in-effect. On the federal front, policy has largely emphasized market-driven supply expansion rather than direct federal construction programs. The focus is on reducing regulatory friction including easing federal environmental review requirements, limiting permitting delays, and reinforcing local control over zoning decisions rather than expanding federal housing mandates.

As I described above, lowering regulatory barriers allows builders to increase housing supply organically, improving affordability through production (increasing supply) rather than subsidy (focusing on cost alone).

The most tangible current housing-adjacent initiative is the expansion of opportunity zones, which provide tax incentives for private investment in designated distressed areas.

Other recent proposals include Freedom Cities, which are new planned communities built on federal land through public-private partnerships, and support for manufactured and modular housing as lower-cost supply solutions. The Freedom Cities and broader manufactured housing reforms are still at the conceptual or proposal levels but could contribute to increased supply.

State level regulation has some of the greatest impact on housing supply. States with some of the most consequential housing supply reforms include California, Oregon, Florida, Texas, and Montana which have enacted measures that preempt restrictive local rules and expand allowable density.

For example, California has legalized lot splits and duplexes, streamlined higher-density approvals, and expanded Accessory Dwelling Unit development so homeowners can add an additional unit or building to their lot. Oregon has eliminated single-family-only zoning in many areas, while Florida’s Live Local Act limits local density constraints on multifamily projects. Texas and Montana have also expanded Accessory Dwelling Units, reduced development fees, and implemented broader zoning reforms. These types of initiatives could have a significant impact on supply by reducing regulatory barriers.

New Innovations. In addition to lower regulation and expanded land use, what and how builders build on that land is advancing with technology. 3D-printed housing is evolving from experimental prototypes to small-scale production with focus now shifting to scalability. Companies are building multi-home developments using on-site robotic concrete printing systems that can complete wall structures in a matter of days. Advances in printable materials, that include high-strength, fast-curing, and lower-carbon concrete blends, are improving durability, insulation performance, and structural efficiency. Instead of the traditional right-angled walls, curved and hollow-core wall designs allow for stronger load distribution, utilities embedded in walls, and reduced material usage. Design-to-print workflows have also become more efficient, speeding up planning and permitting, and customization.

Beyond the individual house, production is shifting toward neighborhood-scale building using a combination of printed and conventional construction. The reduction in labor required to build these houses could also address skilled labor shortages. The big opportunity for printed houses is that builders can be more responsive to land use opportunities and more quickly increase supply.

What Does This Mean for Profitable Revenue Growth? If supply-side regulatory reform and construction innovation begin to meaningfully increase housing production, depending on your industry, it could translate to volume and velocity for your business. Faster permitting, higher allowable density, and streamlined approvals reduce development friction. That means more projects moving forward, more households forming, and more transactions occurring. You should evaluate where regulatory reform is most active and align your geographic investment, sales focus, and partnerships accordingly. States preempting restrictive zoning and accelerating density will likely see increased housing starts before others. For regulation, follow the reform which will lead to increased supply and shifting demand.

On the technology front, if 3D printing, modular systems, and hybrid construction continue compressing build cycles and reducing labor intensity, builders will create inventory faster. Look at how your business may benefit from shorter build timelines. As a result, faster supply growth expands the base of new homeowners, in markets where that supply is expanding, which creates increased demand for financing, insurance, furnishings, appliances, technology, and ongoing services. Plus, if your organization can move further upstream into supply-creation opportunities, rather than waiting for the end consumer opportunities, you may capture additional demand.

Ten Questions About Your Customer Strategy for a Supply Constrained Housing Market. To set your direction, here are ten questions you may ask your organization:

- How dependent is our growth on homeownership levels in our core markets?

- How exposed is our revenue to a continued shift from owner-occupied homes toward rentals or institutional ownership?

- Which customer segments represent the greatest untapped opportunity — first-time buyers, move-up buyers, small landlords, or institutional owners?

- Are we allocating sales and capital toward supply-responsive, high-growth markets — or overexposed to structurally constrained regions?

- Where is migration flowing relative to our sales footprint, and are we positioned accordingly?

- If customers “improve instead of move,” are we positioned to capture renovation and upgrade spending?

- How should we differentiate our offers for homeowners, renters, small landlords, and portfolio buyers?

- How will rising insurance costs and cost volatility influence purchasing behavior in our markets?

- Are we modeling delayed first-time homeownership and structural underbuilding into our demand forecasts?

- What housing Signals will we monitor quarterly — and who is accountable for acting on them?

Your Call to Action

Homeownership is foundational to economic mobility. If supply remains constrained, then affordability remains constrained. And, if affordability remains constrained, commercial revenue growth shifts geographically, structurally, and generationally.

Each of the questions that apply to your organization should prompt valuable conversation and ideas around your business and your customer strategy.

Look at each of the signals we’ve discussed. Then, consider their impact from two perspectives: How will they affect your customers and their ability to grow? How will they affect your business?

Get beyond current state and ask your team where they see the signals projecting ahead and what this means for your organization's profitable growth. Consider each of the questions I've asked, add your own, create a plan, and get into action. Questions for us? Email us at info@salesglobe.com or contact us at SalesGlobe.com.

SalesGlobe is a revenue growth consulting and services firm focused on helping our clients reach their growth aspirations through better solution development and operationalizing to get results.

Founder and Managing Partner at SalesGlobe

“We help companies solve tough sales challenges to connect their sales strategies to the bottom line.”

{kind=link}

{kind=link}

{kind=link}